Welcome to the Breakfast Club, your weekly dose of market insights and trading strategies! Join us live every week at 9 AM ET on Traders Reserve Live, where John Hutchinson breaks down the latest market movements, shares actionable trade ideas, and answers your most pressing questions.

Something is happening inside artificial intelligence that most investors aren’t paying attention to.

While everyone watches Nvidia and argues about whether AI has peaked, the real story is playing out underneath — in the companies building the physical infrastructure that makes all of it work. And last week, Goldman Sachs finally noticed.

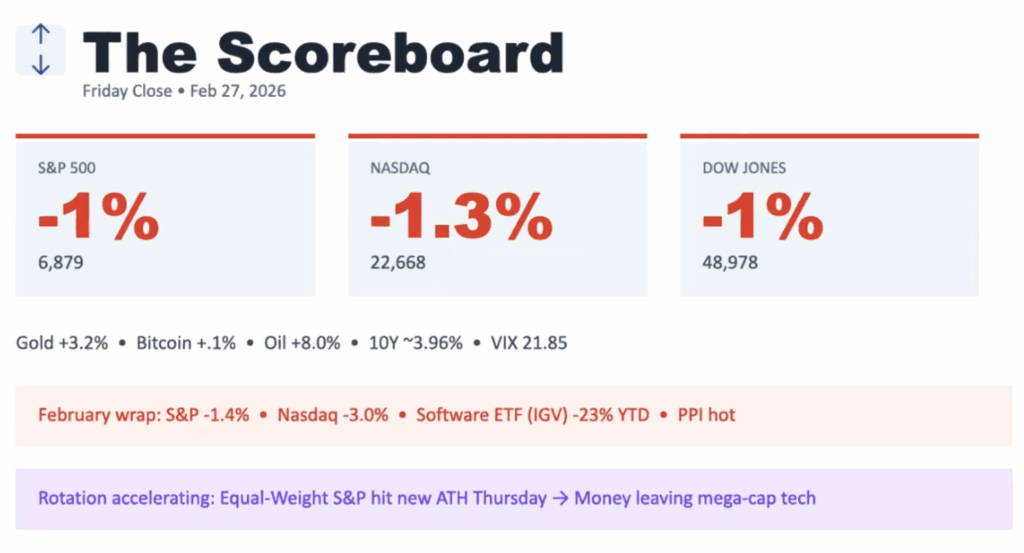

The market closed out February bruised. The S&P fell 1.4% for the month. The Nasdaq dropped 3%. The software ETF — IGV — is now down 23% year to date. Oil spiked 8% overnight on the Middle East conflict. Gold is up 3.2%. And underneath all of it, something interesting: the Equal-Weight S&P 500 hit a new all-time high last Thursday.

That last part matters. It means money isn’t leaving the stock market. It’s leaving mega-cap tech and rotating into everything else. If you’re only watching the Mag 7, you’re watching the wrong index.

Goldman Catches Up

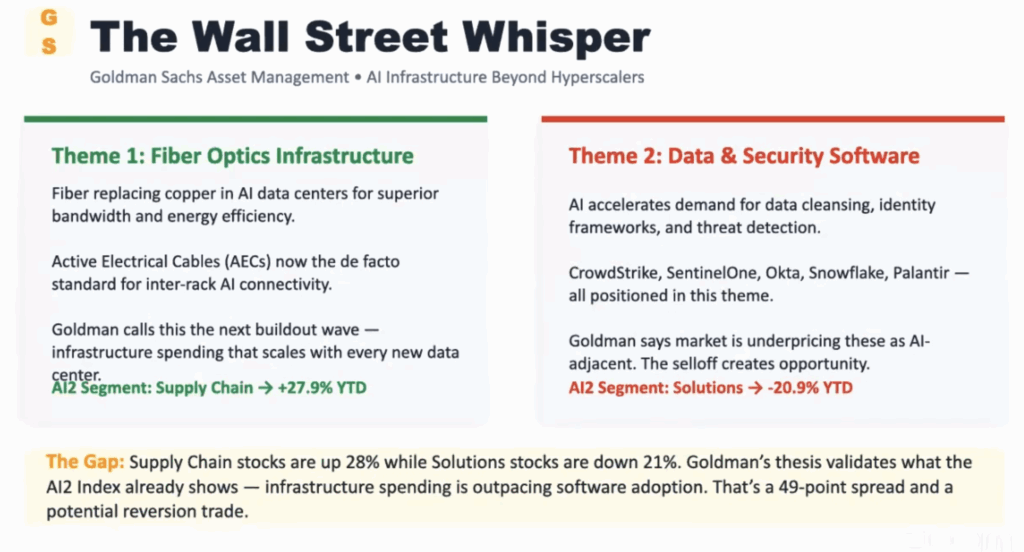

Last week Goldman Sachs Asset Management published a briefing on AI infrastructure opportunities beyond the hyperscalers. Their conclusion came down to two themes: fiber optics infrastructure and data & security software.

If you’ve been following the AI2 Index, you already know this. We’ve been tracking 358 companies across five segments since October. And the data has been telling the same story Goldman just figured out — except we’ve been trading it, not writing reports about it.

Here’s what the gap actually looks like.

Supply Chain stocks in the AI2 Index are up 28.1% year to date. Solutions stocks — which include most of the security and software names Goldman highlighted — are down 21.7%. That’s a 49-point spread between the best and worst segments in artificial intelligence.

Over the last 30 days, Supply Chain was the only segment in positive territory at +7.5%. Core dropped 6.7%. AI-Powered fell 7.6%. Frontier lost 9.6%. And the average EPS growth rate for Supply Chain? 82.6% — more than four times the next closest segment.

This isn’t a close call. It’s a divergence, and it’s widening.

The Stock That Is the Goldman Thesis

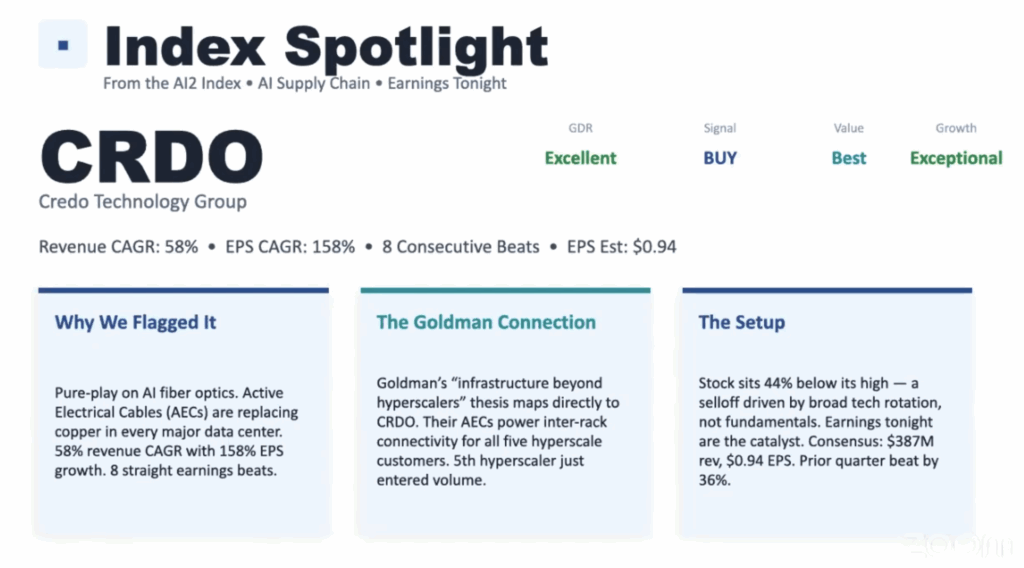

If you wanted to boil Goldman’s entire infrastructure argument into a single stock, it would be Credo Technology Group.

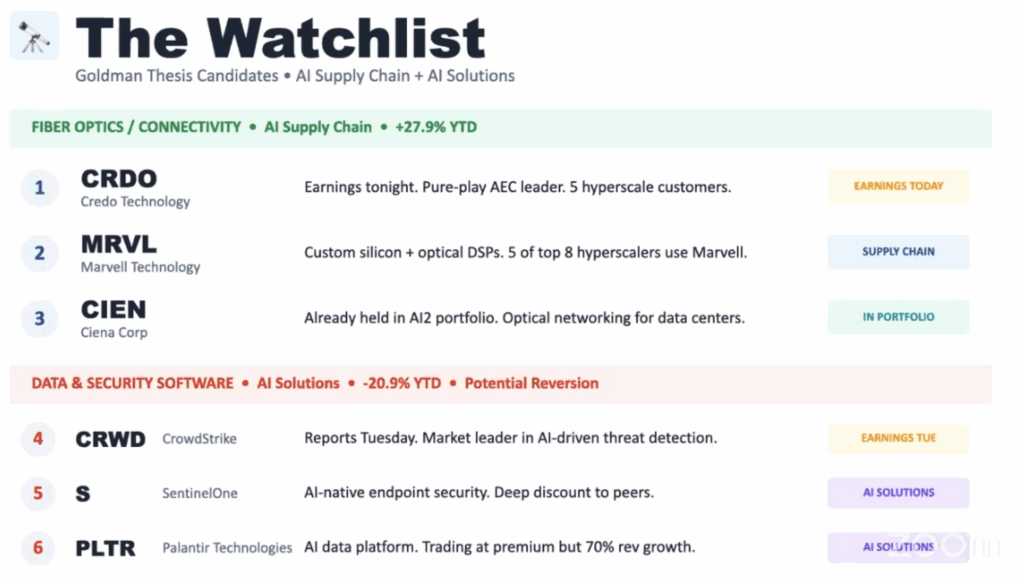

Credo makes Active Electrical Cables — AECs — that are replacing copper in AI data centers. Better bandwidth, better energy efficiency, and they’re becoming the standard for how servers talk to each other inside every major facility being built right now. All five hyperscale customers use them. The fifth just entered volume production.

The numbers are hard to argue with. Revenue is compounding at 58% annually. EPS is compounding at 158%. They’ve beaten earnings eight straight quarters — last time by 36%. Tonight they report again, with Wall Street expecting $0.94 EPS on $387 million in revenue.

And the stock is down 44% from its highs.

That’s not a company falling apart. That’s a company caught in the same broad tech rotation that’s dragged down every growth name since December. At current prices, the AI2 system rates Credo with an Excellent GDR, a BUY signal, Best value rating, and Exceptional growth.

Now — would I rush out and buy this before earnings tonight? No. A stock in a sustained downtrend can pop 15% on earnings and give it all back in a week. That happens more often than people realize, especially in a market that’s punishing companies for not raising guidance fast enough. Wall Street right now doesn’t just want you to beat estimates — they want you to beat them by more than you beat them last time. That’s a high bar.

But if Credo delivers tonight, the setup in the days and weeks ahead gets very interesting. This is one to watch closely.

The Other Side of the Trade

Goldman didn’t just highlight infrastructure. They also flagged security software as undervalued.

Their argument makes sense. Companies aren’t going to hand their entire security infrastructure over to artificial intelligence. As one hedge fund manager put it after the CrowdStrike meltdown last summer — it’s one thing to use AI for your PowerPoint, it’s another to trust it with your firewall.

That creates a floor under names like CrowdStrike, SentinelOne, and Palantir. The problem is timing. These stocks sit in our Solutions segment, which is down 21% year to date. Goldman themselves acknowledge the market is underpricing these as AI-adjacent.

So the question becomes: is a 49-point gap between Supply Chain and Solutions an opportunity or a warning?

If Goldman is right, it’s a reversion trade. Security software is being thrown out with the bathwater while infrastructure keeps climbing. CrowdStrike reports earnings Tuesday. That could be the first test.

If Goldman is wrong — or early — then the gap widens further, and Supply Chain continues to lead.

Either way, the trade is the same right now: follow the infrastructure money.

We’re Still in the Early Inning

The argument that data center spending has peaked doesn’t hold up under scrutiny. If you follow your local news, you’ve almost certainly seen stories about communities pushing back against new data center construction. In southeast Michigan alone there have been multiple lawsuits and organized resistance from residents who don’t want these facilities in their neighborhoods.

That’s the NIMBY problem — Not In My Backyard. And ironically, it’s one of the strongest signals that demand hasn’t peaked. If companies are still fighting to acquire land and build capacity, and if there’s still a backlog on that expansion, then the supply chain companies providing the fiber, the cables, the chips, and the networking equipment have a long runway ahead of them.

Sienna is currently in the AI2 portfolio, up about 12% this month and holding steady even through last week’s sell-off. Lumentum has more than doubled this year — over $600 a share. Corning continues to benefit from the same buildout. Marvell sits at an interesting crossroads — cheap on a forward PE basis, but with a confusing earnings dip projected for next year that needs more clarity.

What to Watch This Week

This is a loaded week beyond Credo. Broadcom reports Wednesday — a major AI2 name. Amprius reports Thursday. On the macro side: ISM manufacturing today, ADP employment Wednesday, jobless claims Thursday, and the jobs report Friday. Retail earnings from Target, Best Buy, Ross Stores, and Costco throughout the week.

And one more thing worth putting on your radar: AI defense stocks. The Middle East conflict is limited in scope — largely an air campaign with a 4-week timeline — but war draws down material, and that material gets replaced. Companies in the AI2 Index that touch artificial intelligence and defense could see a cyclical run over the next 6-12 months. That’s a space I’ll be hunting in.

The bottom line: Goldman’s thesis confirms what the AI2 Index already shows. The AI trade is splitting into infrastructure winners and software laggards. Credo earnings tonight are the Goldman thesis in one stock. Supply Chain is leading. Follow the infrastructure money.

Disclosure: AI2 Insiders holds positions in stocks mentioned in this article. Past performance does not guarantee future results. All investments carry risk.

See What’s Coming at the Conference

I recorded a quick breakdown of the three strategies we’re bringing to Investor’s Blueprint Live on March 20-21 — and the results they’ve already produced this year. Eight minutes. Real numbers. No fluff.