88% in 98 days. 8x forward earnings. 167% earnings growth. And I’m still not selling.

Welcome to the Breakfast Club, your weekly dose of market insights and trading strategies! Join us live every week at 9 AM ET on Traders Reserve Live, where John Hutchinson breaks down the latest market movements, shares actionable trade ideas, and answers your most pressing questions.

There’s a rule every trader hears at some point: don’t fall in love with your stocks.

I’ve said it myself. Probably more than once. It’s good advice. Emotions cloud judgment. Attachment makes you hold too long, exit too late, ignore the warning signs.

So let me be upfront with you — I love Micron.

I know I shouldn’t say that. But when I look at the numbers, the thesis, and the position we’re sitting on right now, I honestly don’t see a reason to pretend otherwise. And I think walking you through exactly why tells a bigger story about what’s happening inside artificial intelligence right now — one that most investors are completely missing because they’re too busy watching Nvidia.

The Trade

We’ve traded Micron twice inside the AI2 portfolio since we launched in October.

The first trade was a 10.8% gain in about 18 days. We got in, the market started to reverse in mid-November, and we pulled out. Disciplined exit. Five days later, we jumped right back in — entry price only about $2 different.

That second trade is still open. And it’s sitting at an 86.4% return over 98 days. Compounded, that’s 106.5%.

Now, we’re not holding a massive position — about 5 shares each time. These are small numbers in dollar terms. But the percentage tells the story. And if you were more heavily invested, this is a company that would have paid off exceptionally well.

Total P&L across both trades: $1,100. Ninety-nine percent of that is in the current position. And I don’t see any reason to exit.

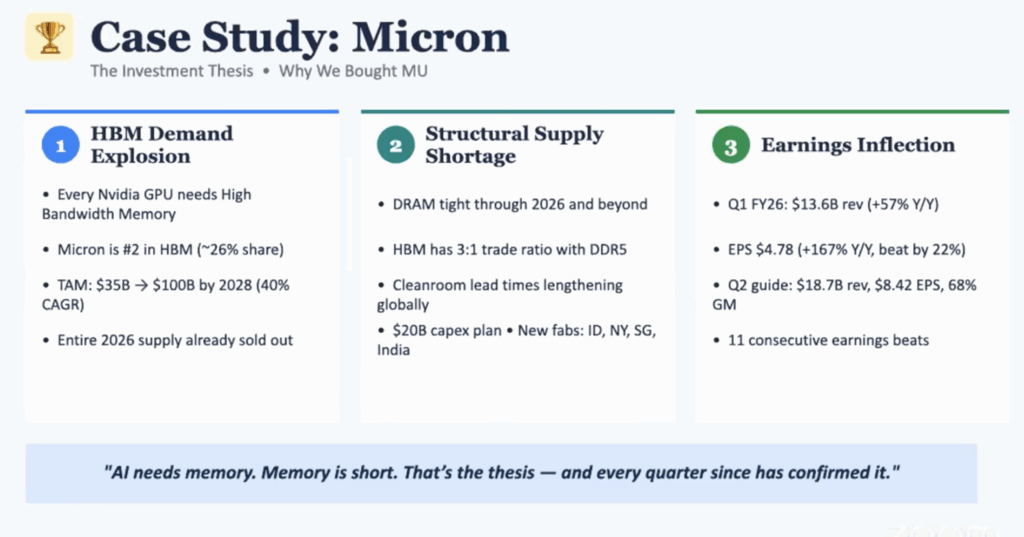

Why Micron Is Still Undervalued

This is the part that I think most people get wrong, and it’s the same mistake I flagged yesterday with Silicon Motion.

When you see a stock that’s already up 88%, the instinct is to assume the move is over. The growth is priced in. You missed it. Move on.

But look at the numbers.

Micron’s earnings growth for fiscal year 2026 is projected at 167% over last year. One hundred and sixty-seven percent. Fiscal 2027 normalizes a bit at 36% — which is still more than triple the S&P 500 average of 10.8%. Even the more conservative 2028 estimates show continued growth, though I have questions about those numbers, which I’ll get to.

And the stock? It’s trading at 8x forward earnings.

Eight times.

That’s not just cheap for a tech stock. That’s PE compression in real time — the stock is literally getting cheaper as earnings rise. Even if the price climbs from here, the earnings growth underneath it is growing faster than the stock price is moving. That’s the definition of undervalued.

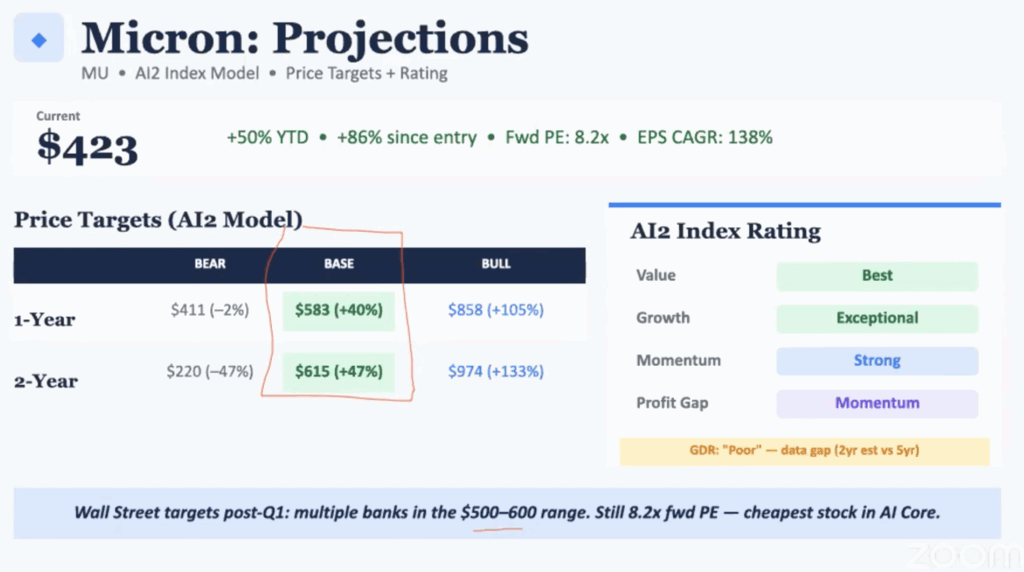

My price target range sits between $580 and $600. Many of the major banks on Wall Street are in that same range. The stock is currently around $215. You do the math.

The Memory Shortage Nobody’s Pricing In

Here’s where the story gets structural.

Back on January 6th, Bank of America published an analyst note that drew attention to a major shortage in memory chip supply. Not a one-quarter blip — a shortage they forecasted to last through 2026 and into 2027.

This is the same catalyst that lit up Silicon Motion, Sandisk, Western Digital, and Seagate Technologies earlier this year. It’s the reason the AI supply chain segment is up 24% while the rest of the index is down 14%. Memory and storage aren’t just participating in the AI buildout — they’re the bottleneck.

Typically, the memory sector is cyclical. You get a 12 to 18-month run, then a downturn, then the next cycle starts. That’s the pattern. And right now, analysts are projecting a potential slowdown in Micron’s revenue by fiscal 2028, which is consistent with them pricing in the end of a cycle.

But here’s what I think they’re getting wrong: if demand is still high and supply is still low going into 2027, that 2028 slowdown number doesn’t hold. Micron just announced a $20 billion capital expenditure plan — new fabrication plants in Idaho, New York, Singapore, and India. That’s not a company managing for the end of a cycle. That’s a company building for sustained, multi-year demand.

And there’s a coverage gap that works in our favor. Only 13 analysts have published 2028 estimates for Micron, compared to 35 for 2026 and 2027. Two-thirds of the analyst community hasn’t weighed in on the forward picture yet. As more coverage comes in, especially after the next earnings report, I expect those numbers to revise upward.

The Bigger Picture

Micron isn’t just a stock pick. It’s a case study in how the AI2 system works.

We look for growth at a discount. We look for companies where earnings are accelerating faster than the stock price. We look for structural demand — not hype, not headlines, but measurable, sustained need for what these companies build.

Micron checks every one of those boxes. The memory shortage provides the demand floor. The $20 billion in capex provides the growth runway. And 8x forward earnings provides the entry point.

Is it perfect? No. The cyclical nature of memory chips means you have to stay alert. The 2028 analyst estimates need watching. And I’ll be the first to tell you that being emotionally attached to a position is a risk in itself.

But sometimes the numbers are so compelling that the rational move and the emotional one happen to point in the same direction. This is one of those times.

I’m holding. And if we get another pullback to the $200 level, I’ll be telling you to add shares.

One More Thing — Nvidia Reports Tonight

Everyone’s going to be watching Nvidia after the close today. And yes, it matters. But here’s what I want you to focus on: forward guidance and free cash flow. That’s what Wall Street cares about right now.

Nvidia will probably beat on earnings — they usually do. But the stock has been range-bound between $175 and $200 since August. A beat alone won’t break that range. What breaks it is raised forward guidance. That’s the holy trinity of earnings: beat EPS, beat revenue, raise guidance. If they hit all three, the stock moves. If they’re conservative on guidance, expect a muted reaction.

And here’s the thing people forget — Nvidia’s real impact isn’t measured on the day of earnings. It’s measured over the next 30 to 60 to 90 days across the entire AI sector. As Nvidia goes, so goes the AI economy. We’ll break down the actual numbers tomorrow.

If you want access to the full AI2 Index — the segment breakdowns, the stock ratings, the real-time portfolio — AI2 Insiders is where it happens. We’re sitting on an 88% open winner and adding new positions this week.

Disclosure: AI2 Insiders holds positions in stocks mentioned in this article. Past performance does not guarantee future results. All investments carry risk.

Want to See This Live? Come to Dallas.

Investor’s Blueprint Live — March 20-21. Five presenters. Two days. Live trading Friday, learning sessions Saturday.

NOW INCLUDING Markay Latimer with her brand new LEAP strategy — bigger moves, less capital, same stocks we’re already trading. $197. Limited live and virtual seats remaining.