Welcome to the Breakfast Club, your weekly dose of market insights and trading strategies! Join us live every week at 9 AM ET on Traders Reserve Live, where John Hutchinson breaks down the latest market movements, shares actionable trade ideas, and answers your most pressing questions.

John Hutchinson opened this morning’s Breakfast Club by naming it directly: Groundhog Day. And he’s not wrong — the pattern has been almost mechanical. Monday rally, weekly fade, repeat.

This is the most important thing I said this morning, and I don’t want you to miss it.

For weeks, every Trump Truth Social post about Iran moved markets. A hint of de-escalation sent futures surging. A threat sent oil higher. We were essentially trading social media in real time — and it worked, until it didn’t.

Last week, it stopped working.

Wall Street is done responding to diplomatic language on a screen. What the market wants now — what it needs — is to see ships actually moving through the Strait of Hormuz. Real movement. Real de-escalation. Until that happens, every Monday rally is borrowed. The rest of the week will keep taking it back.

That’s a meaningful shift in how this market is behaving, and if you don’t adjust to it, you’ll keep getting caught in the same pattern.

Oil is still the headline. But last week added a second headwind that is now running parallel to the Iran conflict — and in some ways, it’s becoming the more dangerous of the two.

The 10-year Treasury yield.

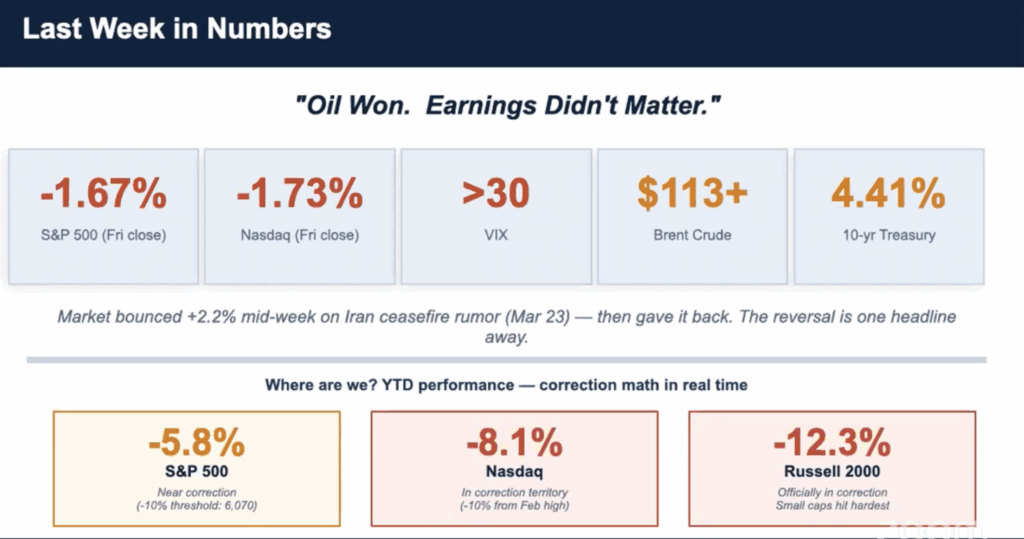

From mid-February to last week, the 10-year yield rose roughly 10% — from around 4% all the way up to 4.41%. That is the bond market telling you something. It’s pricing in inflation staying higher for longer. And a rising 10-year yield is a direct headwind on stock valuations, especially growth stocks and anything in the AI space.

The number I’m watching: 4.5%. If the 10-year gets to 4.5% and stays there, that is a serious structural problem for the market — not just temporary pressure. If instead yields start pulling back from 4.4%, that gives stocks some room.

What’s driving the yield higher? Three things piling up at once: continued oil price pressure, import and export prices jumping to levels not seen since 2022, and two consecutive months of rising Producer Price Index readings. All of it pointing the same direction — inflation isn’t cooling the way the Fed needs it to.

By Friday’s close, the CME FedWatch tool was showing a 50% probability of a rate hike by December. Not a cut. A hike.

That number crushed stocks Thursday and Friday. And I think Wall Street overshot.

Here’s the thing — not one Fed speaker last week said anything close to rate hikes. The Fed dot plot still shows one rate cut likely in Q4. What we have right now is a wide and growing divergence between what the Fed is actually saying and what Wall Street is trying to price in. Wall Street always prices the worst case first. That’s what happened Friday.

Powell was also direct on stagflation: the conditions of the 1970s are nothing like what we’re seeing today. The Fed is not panicking.

So what does that mean for this week? Watch Fed speakers. If they stay on message — patient, data-dependent, no mention of hikes — that 50% December hike probability starts to unwind and some of Friday’s damage gets recovered. One dovish comment from a voting Fed member is all it takes to reset market pricing. That’s the trigger I’m watching most closely this week.

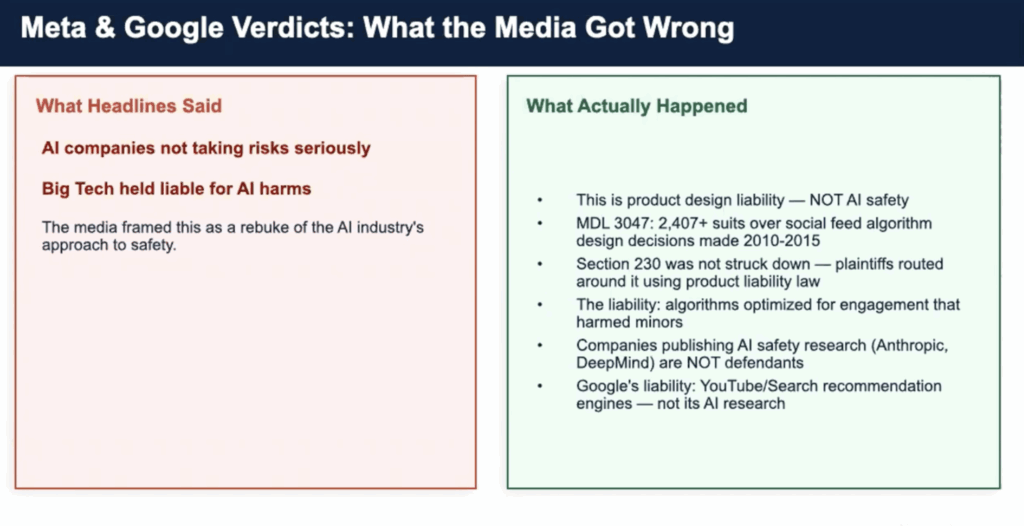

The AI Story the Media Got Completely Wrong

Google and Meta both lost court cases last week. The headlines said AI companies aren’t taking safety seriously. Big Tech held liable for AI harms.

That’s not what happened.

What actually happened was MDL 3047 — 2,407 lawsuits over social feed algorithm design decisions made between 2010 and 2015. Algorithms optimized for engagement that harmed minors. This is product design liability, not AI safety. Section 230 wasn’t struck down. Google’s liability was its YouTube and Search recommendation engines — not its AI research. The companies actually publishing AI safety research — Anthropic, DeepMind — aren’t even defendants in this case.

The media conflated a decade-old product design issue with the current state of artificial intelligence. It knocked a third leg out from under AI stocks last week — but not for any fundamental reason. The long-term thesis hasn’t changed.

The Angle Nobody Is Covering: China

Here’s something I don’t think is getting nearly enough attention.

China imports roughly 75% of its oil through the Strait of Hormuz. The same crisis driving US energy costs higher is simultaneously choking China’s ability to build out data centers and compete on the AI front. VNET — one of China’s major AI data center operators — was up 24% year-to-date earlier this month. It’s now essentially flat on the year.

China is dealing with a dual macro headwind: US-China trade tension plus Hormuz oil disruption hitting at the same time. Gas shortages are already being reported across Vietnam and the broader Asia-Pacific. This is becoming a global economy problem, and it’s going to pressure the AI buildout story on both sides of the Pacific.

But here’s the angle I find interesting: high oil prices make cloud inference more expensive globally. That accelerates the economic case for edge AI and on-device processing — and that’s a tailwind for US-based supply chain names positioned to capture that shift. If you’re looking for places to hunt right now, edge computing and quantum computing are two areas worth putting on your radar.

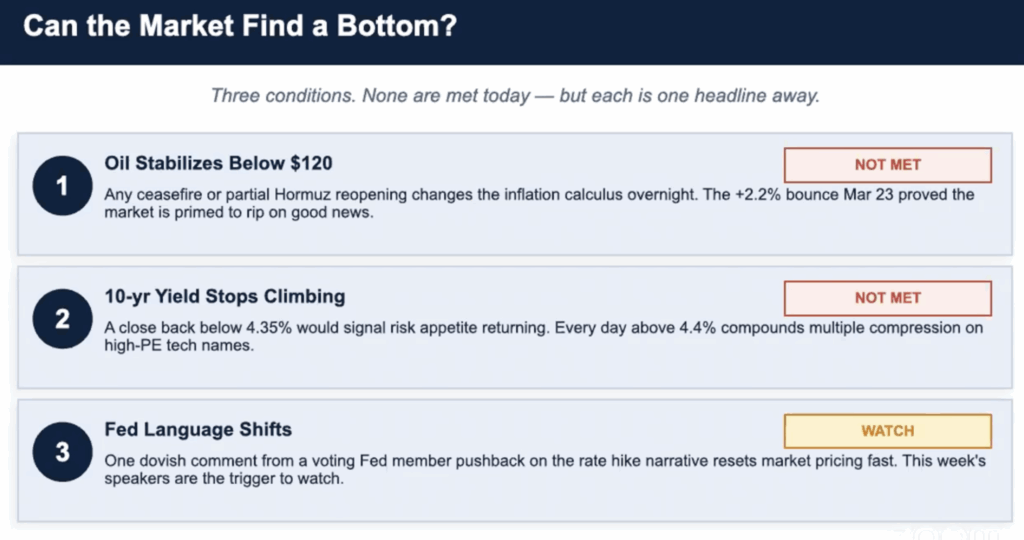

Can This Market Find a Bottom?

Three conditions. None of them are met today — but each one is a single headline away.

Oil needs to stabilize below $120. Any ceasefire or partial Hormuz reopening changes the inflation calculus overnight. The +2.2% bounce on March 23rd proved this market is primed to rip on good news. It just needs the good news to stick.

The 10-year yield needs to stop climbing. A close back below 4.35% would signal risk appetite returning. Every day above 4.4% compounds multiple compression on high-PE tech names — and that includes most of what I’m holding.

Fed language needs to shift. One dovish comment from a voting Fed member pushes back on the rate hike narrative and resets market pricing fast. This week’s Fed speakers are the most important thing to watch.

Until all three start moving in the right direction, my guidance is simple: low and slow. Reduce your exposure. If you normally sell 10 contracts, sell 2 or 4. Don’t go to zero — there are still opportunities in supply chain, memory, and semiconductor names that are bouncing off key levels. But don’t size as if the bottom is confirmed, because it isn’t.

One more thing worth flagging: this is a big data week. The jobs report and ISM services both drop Friday. The catch — markets are closed for Good Friday. Whatever those numbers say, you won’t be able to trade the reaction until Monday. Plan for that now, not after the fact.

Happy Easter. And don’t let Groundhog Day catch you again this week.