116 stocks are up 24%. The rest of AI is down 14%. The difference is everything.

Welcome to the Breakfast Club, your weekly dose of market insights and trading strategies! Join us live every week at 9 AM ET on Traders Reserve Live, where John Hutchinson breaks down the latest market movements, shares actionable trade ideas, and answers your most pressing questions.

I want to show you something that I think most investors are completely missing right now.

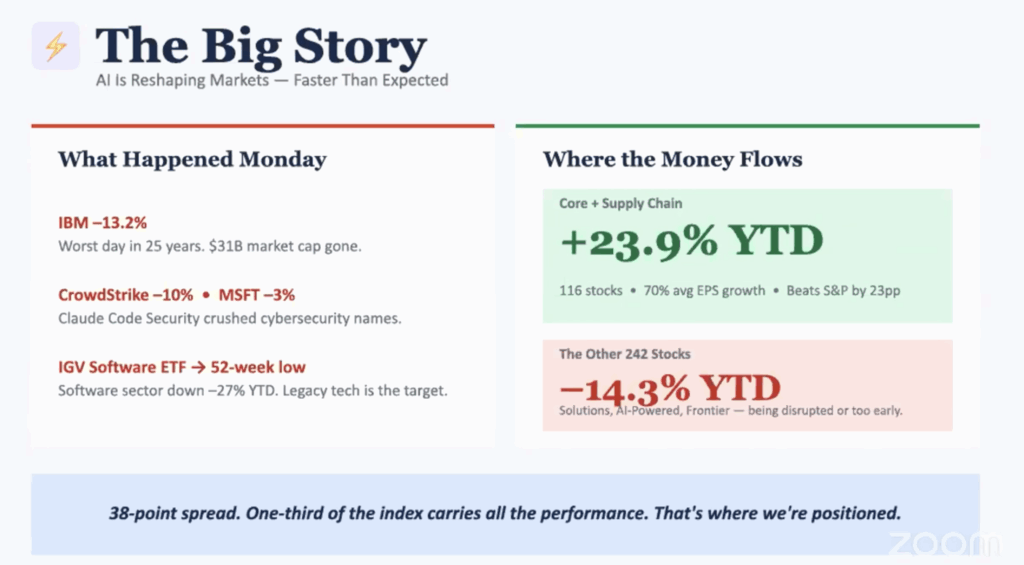

If you just read the news — the headlines, the hot takes, the doom-and-gloom cycle — you’d think artificial intelligence was a bust. IBM lost $31 billion in market cap yesterday. The software ETF just hit a 52-week low. CrowdStrike’s getting hammered. Everywhere you look, it feels like the AI trade is falling apart.

And I get why people feel that way. I do. But they’re looking at the wrong stocks.

Two AIs

I track over 350 companies inside the AI2 Index. And when I pulled the numbers apart last night, the picture that emerged was so stark it almost looked like two completely different markets.

Group one: AI Core and AI Supply Chain. That’s 116 companies. Average return year to date? Up 24%. Beating the S&P 500 by more than 20 points. Average EPS growth is extremely high. These are the companies building, powering, and enabling AI infrastructure — the chips, the memory, the storage, the hardware that every AI application on earth depends on.

Group two: everything else. AI-powered industries, AI solutions, parts of the software stack. Down 14%.

Read that again. One group is up 24%. The other is down 14%. Same index. Same sector. Same “AI.”

That’s not a market correction. That’s a structural divergence. And if you’re not paying attention to which side you’re on, you’re going to have a very frustrating year.

Why Software Is Getting Crushed

Let me be direct about what’s happening. The software sector is under heavy attack right now, and a lot of it traces back to one thing: AI is starting to replace what software companies sell.

When Anthropic announced Claude and the co-work capabilities at the end of January, it sent a shockwave through the software space. CrowdStrike is suddenly being questioned because Claude can apparently handle code security. IBM lost $31 billion because Anthropic demonstrated it could replicate a key IBM program. The cybersecurity names, the enterprise software names — they’re all feeling this pressure.

Now, do I believe Claude can do everything these companies do? No. Not yet. And I wouldn’t panic-sell quality software companies. But the market is repricing risk in real time, and right now, that repricing is brutal for software and services.

Where the Money Is Actually Going

Here’s the thing that the headline readers are missing: the money didn’t leave AI. It migrated within AI.

Capital is flowing into the companies that are building the physical infrastructure — semiconductors, memory, storage, networking, the actual supply chain that makes AI work. These are companies with measurable revenue growth, accelerating earnings, and a demand curve that still hasn’t flattened.

That’s not my opinion. That’s what the numbers say. A 24% average return across 116 companies isn’t a coincidence. It’s a trend. And it’s the trend that’s driving roughly 80% of the positions we currently hold in the AI2 portfolio.

We’re following the money. And it’s paying off.

The Stock That Shows You Why

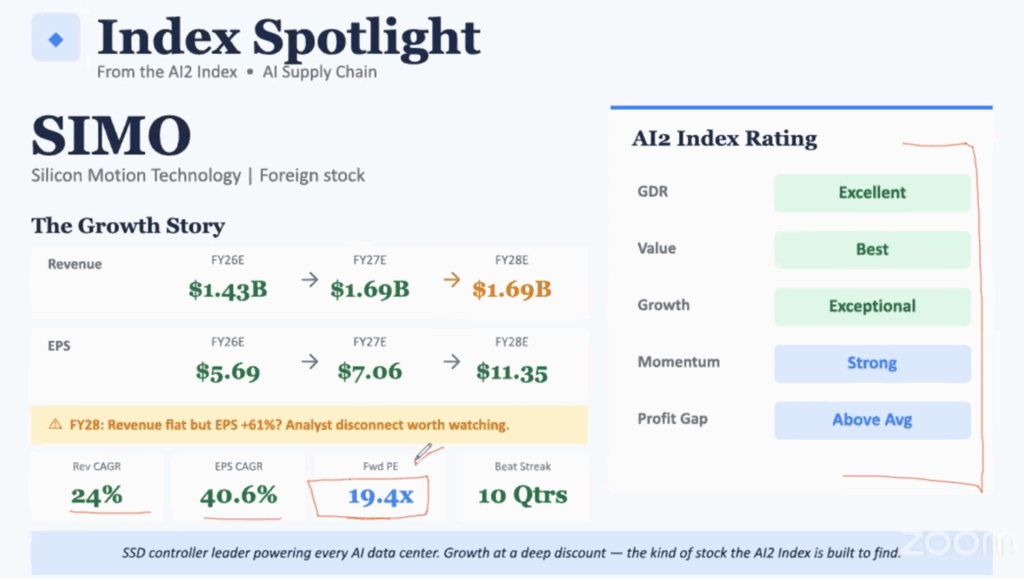

I want to make this concrete with one name: Silicon Motion Technology, ticker SIMO.

This is a company that makes SSD controllers for NAND flash memory. If that sounds technical, here’s the plain version: they make the components that allow data centers to store and retrieve the massive amounts of data that AI needs to function. Without companies like SIMO, the AI infrastructure doesn’t work.

Here’s what the numbers look like:

Revenue growing over 24% annually. EPS growing over 40% — and on a compounded basis, their earnings are projected to essentially double between now and 2028. They’ve beaten earnings estimates for 10 consecutive quarters.

And here’s the part that really got my attention: the stock is trading at 19x forward earnings. For a tech stock with 40% EPS growth. That’s not just cheap — that’s insanely cheap. The S&P 500 average EPS growth this year is 10.8%. SIMO is operating at four times that rate, and the market still hasn’t fully priced it in.

Now I know what some of you are thinking — the stock is already up 125% in the last 12 months. All the growth must be behind it. Right?

Wrong. And this is a mistake I keep seeing investors make across the AI space.

Just because a stock has run doesn’t mean all the growth is priced in. The profit gap — the difference between where the price is today and where earnings say it should be — is still above average on SIMO. My base case puts the stock somewhere between $167 and $269 over the next 12 months. That’s a potential near-double from current levels around $136.

Wall Street’s analyst targets are all over the place — a $27 spread from the low estimate to the high. That tells me the street hasn’t caught up yet. And when a stock has been beating for 10 straight quarters and the analysts still can’t agree on a target, that usually means there’s more upside than they’re pricing in.

The chart backs it up. Long uptrend from $40 last year. Clean breakout. New highs since 2022. And the volume surge since January — especially those two big green bars that coincided with the Bank of America report on the memory shortage — tells me institutional money is coming in.

It even pays a dividend, if that matters to you. Just be aware it’s a foreign company, so check with your advisor on tax implications.

What This Means for You

Look, I’ll be honest. My biggest frustration right now is that there are too many good names and not enough capital to own all of them. If I were running a $10 billion hedge fund, I’d own all 116 stocks in core and supply chain. As a retail investor, you have to be selective. That’s the reality.

But here’s what I want you to take away from this: if you do nothing else, focus your attention on AI Core and AI Supply Chain. Those two segments are where the winners are. The data says so. The performance says so. And the earnings trajectory says so.

The doom-and-gloom headlines are about a different part of the AI economy. Don’t let them scare you out of the part that’s actually working.

If you’re not inside AI2 Insiders, you’re not seeing the segment-by-segment breakdowns, the stock ratings, or the portfolio moves in real time. We’re up over 15% in 6 weeks — not because we’re lucky, but because we know where to look.

Disclosure: AI2 Insiders holds positions in stocks mentioned in this article. Past performance does not guarantee future results. All investments carry risk.

If you want access to the expanded rankings, weekly scoring updates, and early model changes, you can join AI2 Insiders here.

Join our trading community and get access to the tools, data, and strategies that are helping us win week after week. Join Traders Reserve today.