Welcome to the Breakfast Club, your weekly dose of market insights and trading strategies! Join us live every week at 9 AM ET on Traders Reserve Live, where John Hutchinson breaks down the latest market movements, shares actionable trade ideas, and answers your most pressing questions.

Last Monday morning, the Wall Street Journal published a story about OpenAI.

It talked about missed user goals, unsustainable spending, competition from Anthropic, Perplexity, and Manus. Real concerns about a specific company with a pending IPO. Legitimate journalism about one player in the AI space.

Wall Street read it as a verdict on the entire artificial intelligence industry. Tech stocks sold off Monday. Tuesday was worse.

I got mad. And when I get mad, I buy.

Here’s what actually happened last week — and why the WSJ is going to have to eat those words.

The Week in Five Days

Friday April 24th: AI2 portfolio sitting at +49% on cost. +75% YTD.

Monday April 27th: WSJ story drops the same morning as our Breakfast Club deck. Market sells off.

Tuesday April 28th: Portfolio drops to +33% on cost. The trough. I sent the discount-day alert and backed our own positions.

Wednesday April 29th: Hyperscalers report after the bell. Everything changes.

Thursday April 30th: SIMO and MXL earnings amplify the recovery.

Friday May 1st: Book closes the week at +50% on cost. +90% YTD.

Sixteen points off in two days. Seventeen points back on in three. That’s the shape of the week.

Why I Bought on Tuesday

I’ll tell you what I told AI2 members on Tuesday afternoon: if you want to buy Lumentum at the best price you’re going to get in the last 40 days, today is the day.

I was right.

Here’s my reasoning — and it wasn’t complicated. I looked across every stock we hold. The fundamentals hadn’t changed. The thesis hadn’t changed. What changed was a news story about one company that Wall Street incorrectly extrapolated to an entire sector.

Wall Street sells first and asks questions later. Then they go to lunch, come back, and realize the story doesn’t make any sense. And then they bid everything right back up.

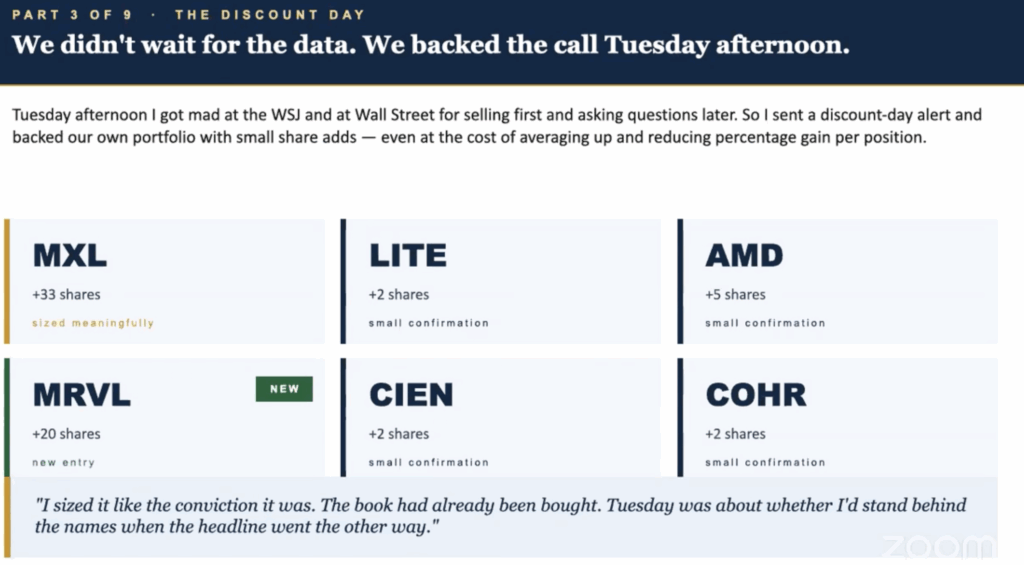

So I added 33 shares of MXL. Two shares of Lumentum. Five shares of AMD. Two each of Ciena and Coherent. And I opened a new position in Marvell Technology — an ancillary optical supply chain name that reports earnings later this month.

I sized it like the conviction it was. Tuesday was about whether I’d stand behind the names when the headline went the other way.

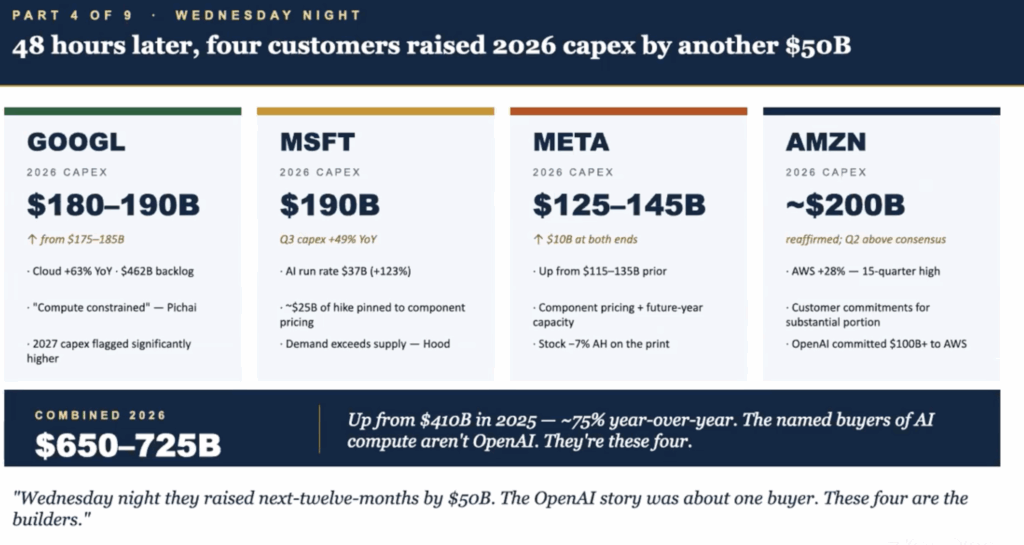

Wednesday night, four companies reported earnings. Google, Microsoft, Meta, Amazon.

Combined 2026 AI capital expenditure: $650–$725 billion. Up from $410 billion in 2025. A 75% year-over-year increase. In a single earnings evening, the named buyers of AI compute raised their next-twelve-months spend by $50 billion.

The WSJ story was about one buyer — OpenAI. These four are the builders.

Google said they’re “compute constrained.” Microsoft pinned roughly $25 billion of their capex increase directly to component pricing — meaning suppliers can’t keep up with what they need. Meta raised both ends of their guidance by $10 billion. Amazon reaffirmed ~$200 billion with AWS up 28% — a 15-quarter high.

Microsoft also shared that their AI run rate is growing at 100% per year. That’s not a narrative. That’s the number.

By Wednesday night, the “AI spending is slowing” story was dead. And the stocks — our stocks — started moving.

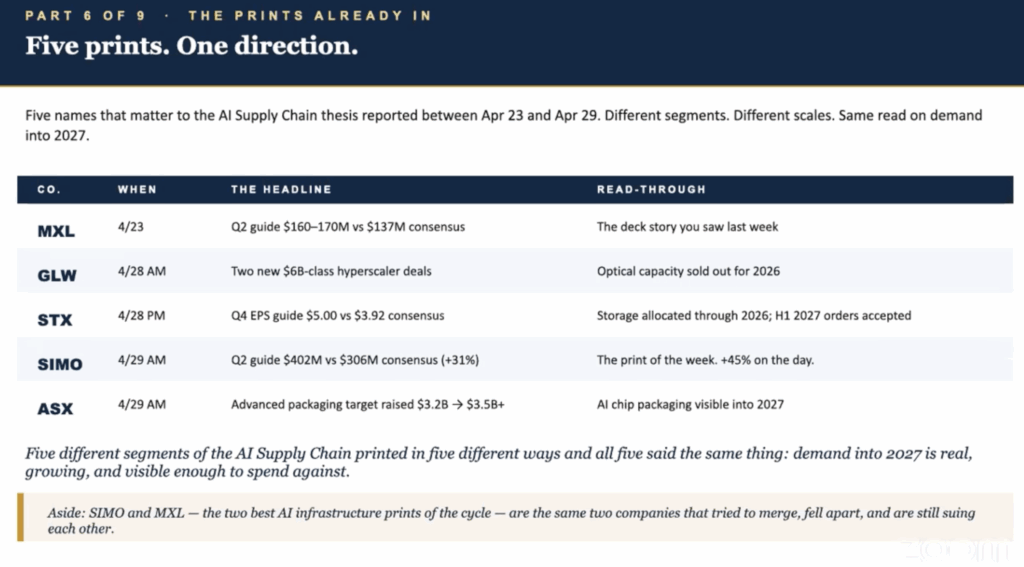

Between April 23rd and April 29th, five companies directly tied to the AI supply chain reported earnings. Different segments. Different scales. Same read on demand into 2027.

MaxLinear guided Q2 at $160–$170 million versus a $137 million consensus. Corning announced two new $6 billion hyperscaler deals and said optical capacity is sold out for 2026. Seagate raised Q4 EPS guidance from $3.92 to $5.00 — a 20% increase — and said storage is allocated through 2026 with H1 2027 orders already accepted. Silicon Motion guided Q2 at $402 million versus a $306 million consensus, a 31% beat, and the stock gapped up 45% on the print. ASE Technology raised advanced packaging targets from $3.2 billion to $3.5 billion with AI chip visibility now extending into 2027.

Five different segments of the AI supply chain. Five different ways of saying the same thing: demand into 2027 is real, growing, and visible enough to spend against.

One sidebar worth noting: SIMO and MXL — the two best AI infrastructure prints of the entire cycle — are the same two companies that tried to merge a couple of years ago, fell apart, and are currently suing each other. I think they should just walk away from that lawsuit. Both companies are doing just fine on their own.

The Generational Build-Out Nobody Is Pricing Correctly

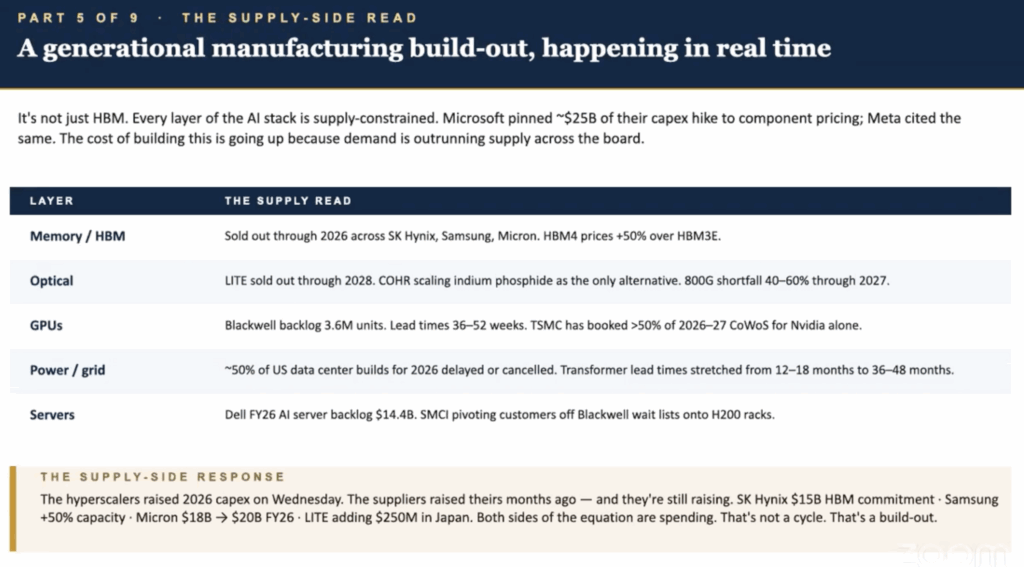

Here’s the bigger picture. It’s not just one layer of the supply chain that’s constrained. It’s every layer.

Memory and HBM: sold out through 2026 across SK Hynix, Samsung, and Micron. HBM4 prices are running 50% above HBM3E.

Optical: Lumentum sold out through 2028. Coherent is scaling indium phosphide as the only alternative. 800G shortfall running 40–60% through 2027.

GPUs: Nvidia’s Blackwell backlog at 3.6 million units. Lead times of 36–52 weeks. TSMC has booked more than 50% of 2026–27 CoWoS capacity for Nvidia alone.

Power and grid: roughly 50% of US data center builds for 2026 are delayed or cancelled — not because of lack of demand, but because transformer lead times have stretched from 12–18 months to 36–48 months. You can’t build a data center without a transformer.

Servers: Dell’s fiscal year 2026 AI server backlog is $14.4 billion.

The hyperscalers raised 2026 capex Wednesday. The suppliers raised theirs months ago — and they’re still raising. SK Hynix at $15 billion HBM commitment. Samsung adding 50% capacity. Micron raising capex from $18 billion to $20 billion. Lumentum adding $250 million in Japan.

Both sides of the equation are spending. That’s not a cycle. That’s a build-out.

I’m calling this a generational manufacturing shift in technology. It’s not priced into the stock market the way it should be. It was not anticipated in the way it’s playing out. And it will run much further in time than most people currently expect.

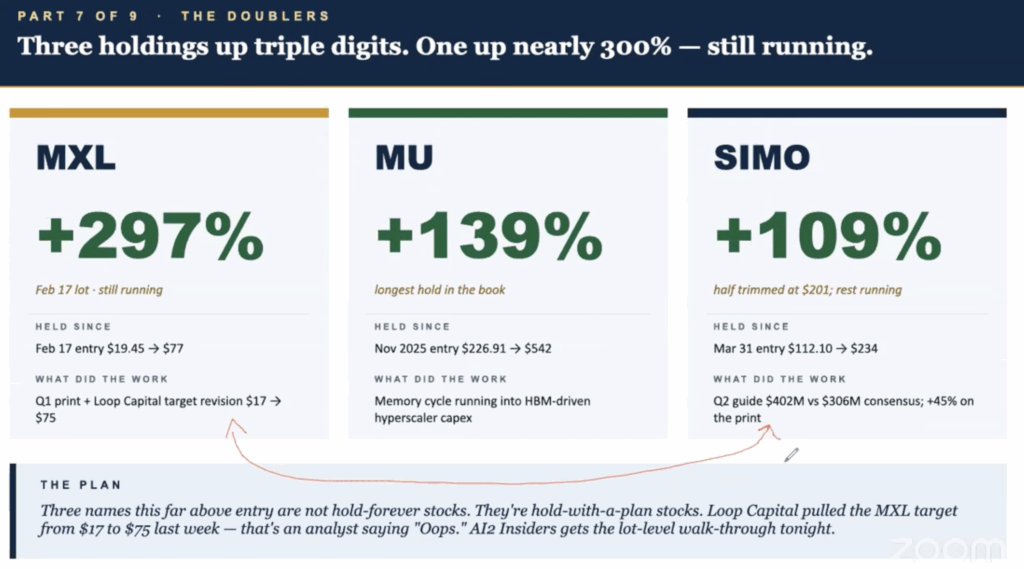

Three Holdings at Triple Digits

MXL: +297%. Entered at $19.45 in February. Now at $77. Still running.

Micron: +139%. Our longest hold, entered in November 2025 at $226.91. Now at $542. I still see this stock in the $800s by end of year.

Silicon Motion: +109%. Entered March 31st at $112.10. Now at $234. Half trimmed at $201, rest still running.

Three names this far above entry are not hold-forever stocks. They’re hold-with-a-plan stocks. Loop Capital pulled their MXL target from $17 to $75 last week — that’s an analyst saying “oops.” The lot-level walk-through on all three is tonight at the AI2 briefing.

What I’m Watching This Week

Five AI2 holdings report earnings in the next three days.

Lumentum Tuesday before the open: optical print after Corning set the bar. I’m watching the 800G/1.6T product mix and hyperscaler concentration.

AMD Tuesday after close: the OpenAI 6GW warrant deal is the binary risk. Will they be cagey or direct on non-OpenAI demand?

Coherent Wednesday after close: cleanest pure-play optical name in the book. Datacom segment growth and Q4 guidance are the two numbers.

KLIC Wednesday after close: the bonder side of the ASX advanced packaging trade. Equipment orders confirm or deny.

Amprius Thursday: wildcard. Small-cap battery name. SiCore platform mix and gross margin trajectory. We’ve been in it since $11. It’s at $21. They may return to profitability this year earlier than projected — if they do, this stock moves fast.

The frame: if LITE, COHR, and KLIC print like SIMO and ASX, the AI supply chain re-rating is structural, not sympathetic. If they don’t, I’ll tell you Friday.

Portfolio is at +90% YTD. Open unrealized P&L over $21,000 on $42,000 invested. We’re going to keep at it.

AI2 briefing today at 4pm. Next Breakfast Club: Monday, May 11th