Welcome to the Breakfast Club, your weekly dose of market insights and trading strategies! Join us live every week at 9 AM ET on Traders Reserve Live, where John Hutchinson breaks down the latest market movements, shares actionable trade ideas, and answers your most pressing questions.

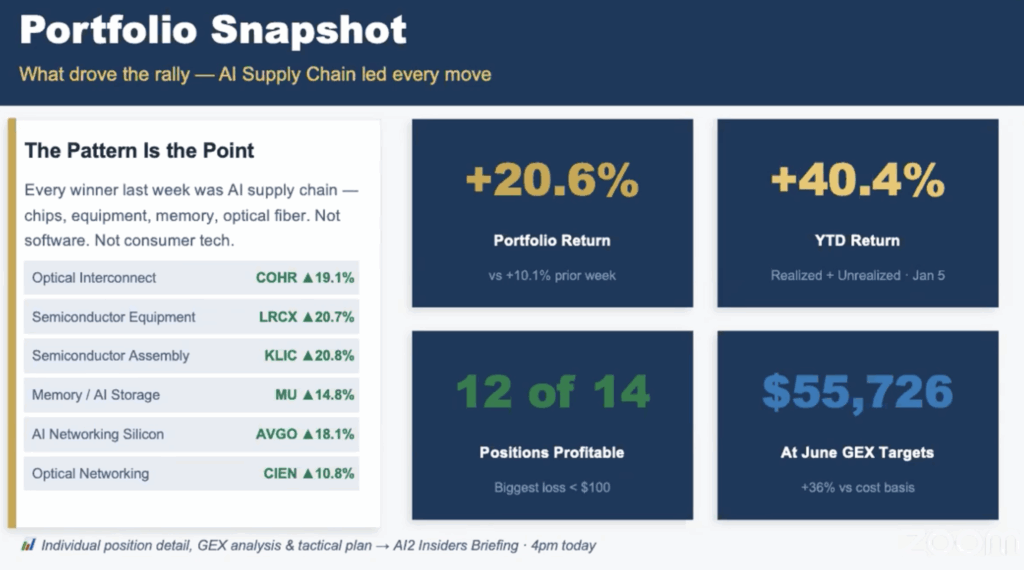

We walked into last week with an 11% gain in the AI2 portfolio. We walked out with just over 20%. That’s on top of a position we closed for a 64% return in roughly 50 days. Year to date, the AI2 portfolio is now at 40.4%.

I’m not saying that to brag. I’m saying it because I think a lot of you are nervous right now — justifiably so — and I want to show you that even in the middle of a ceasefire that nobody trusts, oil bouncing back above $100, and consumer sentiment hitting a 45-year low, there are still stocks going up. Substantially.

The ceasefire was announced Tuesday evening. Wednesday was a broad rally — everyone participated. But then something interesting happened.

Thursday shifted to consumer and financial stocks. Friday brought a very strong semiconductor rally while the rest of the market was down. So even on a bad day for the broader market, the AI supply chain names were green. That’s not luck. That’s what happens when you own stocks with a fundamental reason behind them.

Coherent up 19.1%. Lam Research up 20.7%. KLIC up 20.8%. Broadcom up 18.1%. Micron moved from roughly $320 at the start of the week to nearly $420 by Friday. A hundred dollar move in one week.

Lumentum — ticker LITE — has run from $300 to $900 in four months. That’s not a typo.

These aren’t being headlined on any of the major financial news sites right now. They are quietly leading the market. And that’s exactly where I want to be.

PCE and CPI both came in toward the high end last week. Wall Street largely looked past them — they expected it, they know it’s largely driven by the Iran conflict, and they know it’s temporary. That’s not the report I want to talk about.

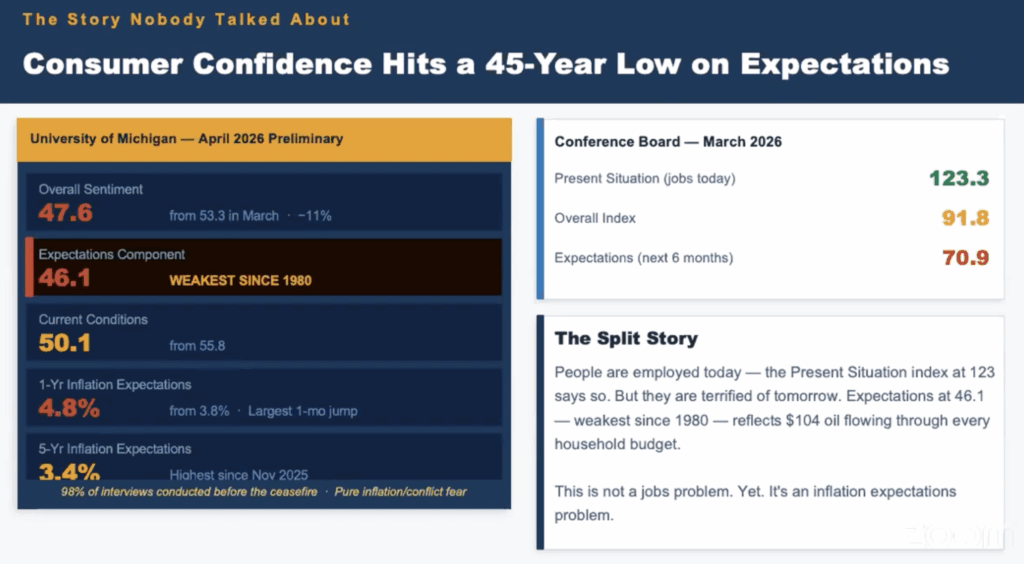

The one I want to talk about is the University of Michigan consumer sentiment report.

Overall sentiment came in at 47.6, down 11% from March. The expectations component — how consumers feel about the next six months — hit 46.1. That’s the weakest reading since 1980. One-year inflation expectations jumped from 3.8% to 4.8%, the largest single-month jump in recent history. Five-year inflation expectations are at 3.4%, the highest since November 2025.

Here’s the split story that matters: people are employed right now. The present situation index at 123.3 says so. But they are terrified of tomorrow. That $104 oil is flowing through every household budget, and they feel it.

This is not a jobs problem yet. It’s an inflation expectations problem. And if you watched what happened in early 2025 — it was a University of Michigan consumer sentiment report that sent markets negative before they ultimately recovered. One data point. Watch it. If it becomes two, it becomes a problem.

The reason the semiconductor names held up on Friday while the rest of the market fell on this report is important: AI infrastructure demand doesn’t move with consumer sentiment. A data center doesn’t get canceled because gas hits $5 a gallon. It costs more to run, but it doesn’t stop. That’s the sector you hide in when consumers are scared.

Dave closed 9 positions last week in Income Masters. Every single one profitable. $1,617 in cash generated across those trades, averaging $180 per position, with an average hold time of 7.3 days.

I did beat him 7 to 1 on overall dollar return last week — AI2 was up roughly $7,500 versus his $1,600. I’ll take the cookie on that one. But what Dave’s results show is that even in the most volatile market we’ve seen in years, a systematic approach to short-term income generation can still work. Same framework, week after week. That consistency matters.

What I’m Watching This Week

Oil is back above $100. That’s the number one thing to watch. If WTI stays above $100 through Wednesday, the stagflation narrative comes back with force. If it falls back below $95, the rally resumes and broadens. Simple as that.

The ceasefire is holding for now. The Strait of Hormuz is still blockaded — call it what you want. Trump posted over the weekend about blockading it further, which is essentially saying the obvious. I think it’s a negotiating tactic. Whether Wall Street overreacts to that like they did in late March is the real question.

Earnings season starts in earnest this week. Goldman Sachs already reported this morning and beat. JPMorgan, Citi, Wells Fargo, Bank of America, and Morgan Stanley all report this week. Then we get into the real test — Microsoft and Google in the next two weeks. Those are two of the largest AI capex spenders on the planet. Microsoft has been under pressure for months on concerns about how much they’re spending on AI. What I’ll be listening for from both of them is two words: supply constrained. That phrase means demand is outpacing what they can build. That’s the signal that keeps the AI supply chain thesis running.

Options open interest for the April 17th expiration is unusually heavy across a wide range of stocks. Once those expire Friday, institutions start pricing forward for next quarter — and that typically eases individual stock volatility. Between this week and next, I think we start to see something closer to normal.

The AI buildout isn’t slowing down. Goldman Sachs said it directly — the Iran conflict doesn’t change the direction or magnitude of AI infrastructure spending. The dollars are already contracted. The demand is already outpacing supply. That doesn’t reverse because of a temporary oil spike.

I don’t think there’s anybody on Wall Street beating me right now. I’ll say it that way. And I think the second quarter sets up to be very good.

AI2 briefing today at 4pm. Next Breakfast Club: Monday, April 20th.